PF Withdrawal Agents Near Me - Best PF Consultant

India's trusted PF withdrawal agents near me - Our Provident Fund consultants assist PF withdrawal, Transfer, Pension & PF Claim issues.

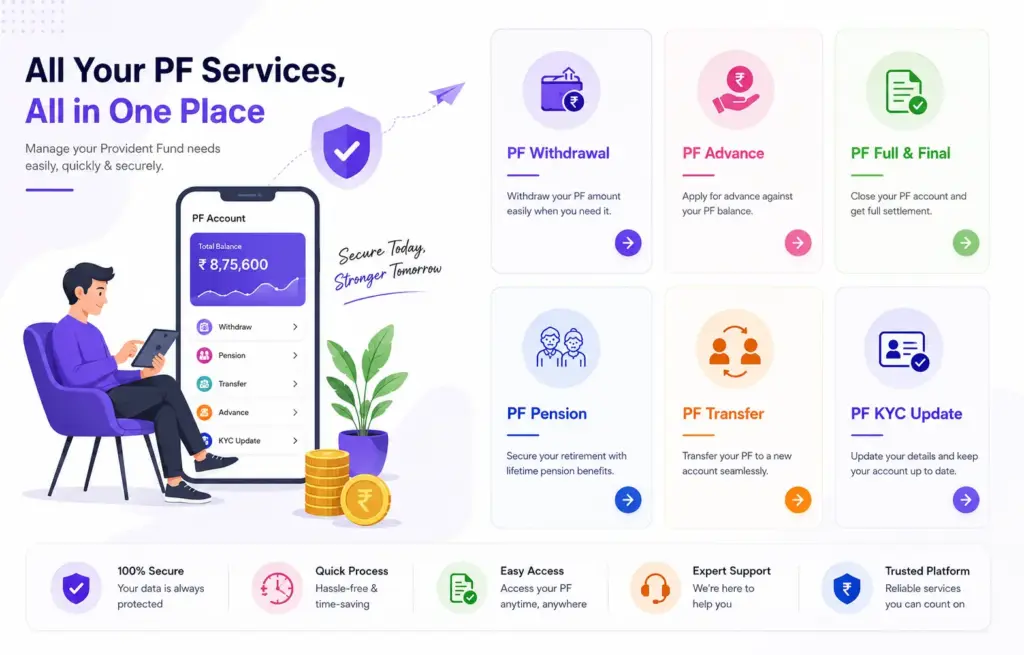

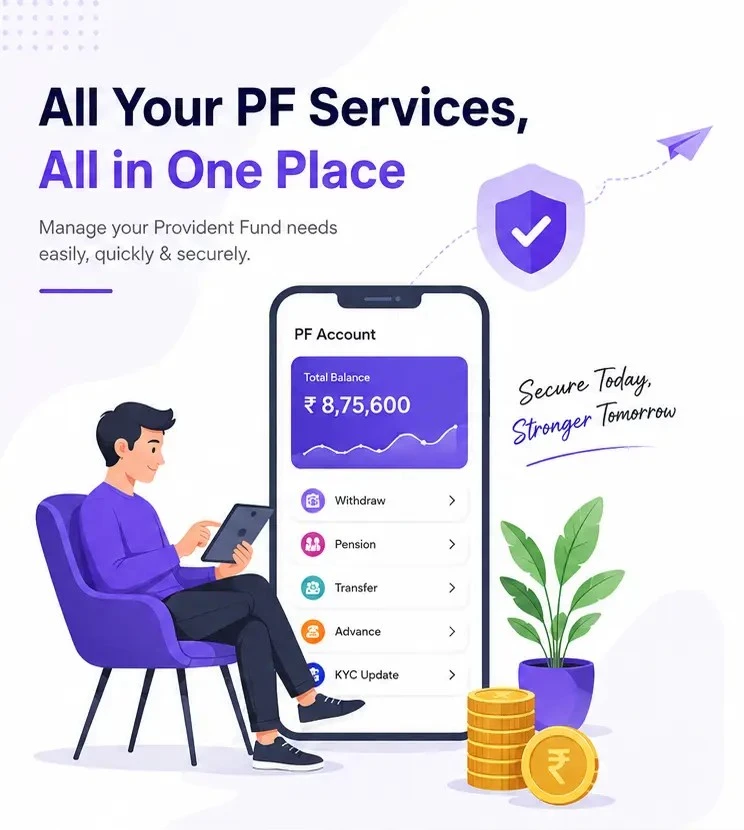

PF Withdrawal

EPF Transfer

PF Pension

Correction of PF

EPF Withdrawal Assistance by PF Withdrawal Agents

Access your provident fund / EPF Withdrawal with ease through our expert PF consultant. We ensure a hassle-free process, guiding you every step for quick and secure claim settlements. Whether it’s a partial or complete withdrawal

Any Type of EPF/ PF Withdrawal Related issue Contacts our Expert Online PF Consultant Number - 8001 044 044

Your Query & Our Solution:

Get in Touch

Send us a message

You can send us a message with details about the issue:

Complete PF Withdrawal Services Under One Roof

Our PF consultants provide end-to-end assistance for various EPF-related services, including:

Why Do PF Claims Get Rejected?

Why Choose Our PF Withdrawal Consultants?

Our objective is not simply to submit an application but to help clients complete the entire process correctly. We focus on understanding the root cause of PF claim issues and providing practical solutions based on EPFO guidelines.

CUSTOMERS SATISFACTION

Whether your claim has been rejected once or multiple times, our experts work to identify the underlying issue before proceeding further.

Connect With PF Consultant

Online PF Consultant - Get Professional Help for Your EPF Claim

You no longer need to search endlessly for a PF consultant near me. Our online consultation service allows employees from every state in India to receive professional assistance without visiting an office. Simply share your issue with our team, and we'll evaluate your case, explain the available options, and guide you through the next steps.

Our services are suitable for salaried employees facing issues such as delayed PF claims, employer-related complications, KYC corrections, UAN problems, EPF transfers, pension claims, and account updates.

If your PF claim is pending, rejected, or delayed, professional guidance can save valuable time and help prevent repeated mistakes. Our experienced PF withdrawal agents assist individuals with documentation, verification, claim guidance, and problem resolution so they can complete their EPF process with greater confidence.

India's No.1 PF Consultant

50,000+ Customer Served

5 Star Rating

Frequently Asked Questions about PF Withdrawal Services

Find quick answers to the most common questions about PF Withdrawal & Transfer and how it can help you.

Yes, EPF contributions are eligible for tax deductions under Section 80C of the Income Tax Act. Employees can claim a deduction of up to ₹1.5 lakh per financial year for their EPF contributions. Additionally, the interest earned on EPF is generally tax-free if the employee continues employment for at least five years.

Employees can withdraw their EPF balance through the EPFO online portal using their UAN login. The process involves logging into the EPFO member portal, selecting the online claim option, choosing the withdrawal type, and submitting the request with bank verification. Once approved, the amount is usually credited to the employee’s bank account within 7–15 working days.

If the PF withdrawal request is still under process, employees can request cancellation through the EPFO grievance portal or by contacting their employer. However, once the claim has been processed by EPFO, it usually cannot be cancelled. In such cases, employees must wait for the amount to be credited to their bank account.

If the status shows “Claim Settled” but the amount has not been credited, employees should first verify their bank account details linked with UAN. Sometimes the payment may take 2–3 additional working days after settlement. If the issue persists, you can check the payment details in the passbook or submit a complaint through the EPFO grievance portal.

Generally, the following documents are required for PF withdrawal:

UAN (Universal Account Number) activated

Aadhaar card linked with UAN

Bank account details linked with UAN

PAN card (for higher withdrawal amounts)

Cancelled cheque or bank passbook copy

These documents help EPFO verify identity and process the claim smoothly.

According to EPFO rules, employees can withdraw their PF balance under certain conditions such as unemployment for more than two months, retirement, medical emergencies, marriage, or house construction. Full withdrawal is usually allowed after retirement or if the employee remains unemployed for a specified period. Partial withdrawals may also be allowed for specific purposes under EPFO guidelines.

Have a question or want more information? We are here to help!